My Teeny Tiny Conference About Milton Friedman

The Fitzwilliam seminar on economic thought

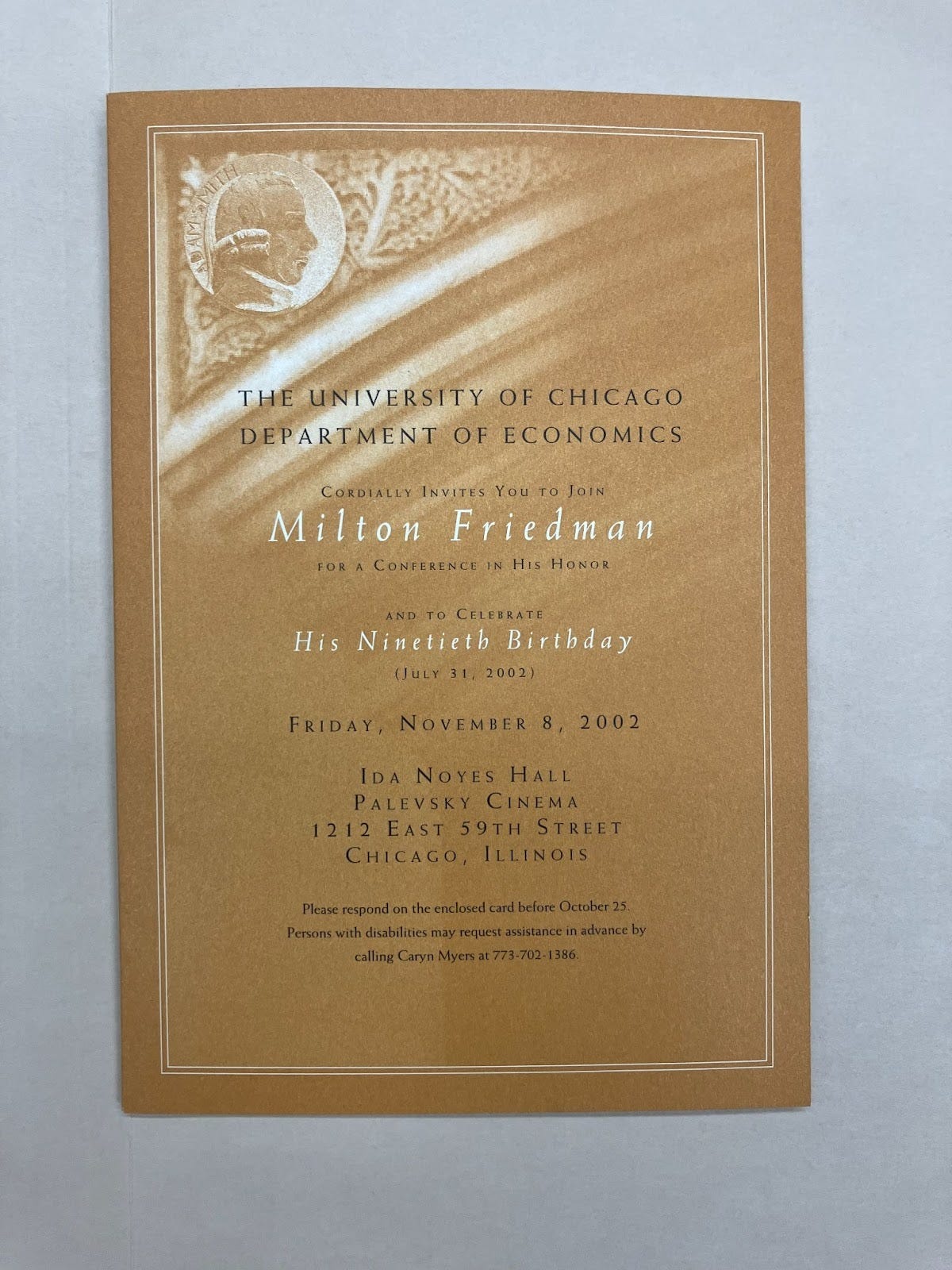

In October last year, I visited Chicago for the first time. I thought that trip would be a good opportunity to run a sequel to the Fitzwilliam conference about Adam Smith that we ran in 2024. I had long wanted to understand the influence of Milton Friedman and the ‘Chicago school’ within economics.

The official title we gave it was ‘The Fitzwilliam Seminar on the History of Economic Thought’. It was hosted at the Quadrangle Club, a spiffy faculty club on the University of Chicago’s campus in Hyde Park.1

My idea was to invite around twelve of my favourite thinkers in economics, philosophy, and intellectual history to show up on a Saturday, for a full day of focused group discussions about the life and thought of Milton Friedman. The event was divided into six sessions, of which I led one.

This format is my favourite way to learn about new topics. It’s great to have a commitment device to force you to read intensely in a given cluster,2 and you make intellectual progress remarkably quickly in the sessions if you have a “no dumb questions” policy. When I sent him a picture from my Friedman event, a friend messaged to say that I already lead his ideal post-AGI life. I suppose I can choose to take that as a compliment that I’ve achieved Aristotelian eudaimonia, or an insult that I don’t do any real work.

To get everyone up to speed, I assigned both general background reading, and also session-specific readings. For general background, we read chapter two of Tyler Cowen’s book GOAT: Who is the Greatest Economist of All Time and Why Does it Matter?3 I also nudged people toward reading Jennifer Burns’s biography from 2023.

Overall, I’m happy with how the event turned out. But in future, I’d like to run meetups that are focused on narrower questions, or for which there is more of a cumulative progression throughout the event in understanding a particular text or thinker. Friedman’s life was a bit eclectic for this to work.

This post is made up of my personal notes and reflections from each of the sessions; the presenters wouldn’t necessarily endorse every word. Naturally enough, the programming at a conference is often secondary to getting interesting people in a room together and talking to one another. We had lunch and dinner at Hyde Park classics Medici on 57th and Ascione Bistro, respectively.

Before the event, Matt Teichman also toured me around the University of Chicago’s archives, which contain some of the most historically significant artefacts in the modern history of economics. Most big research universities have absolute gems gathering dust in ‘special collections’, which I strongly recommend visiting. I’ll include some photos I took during my visit there.

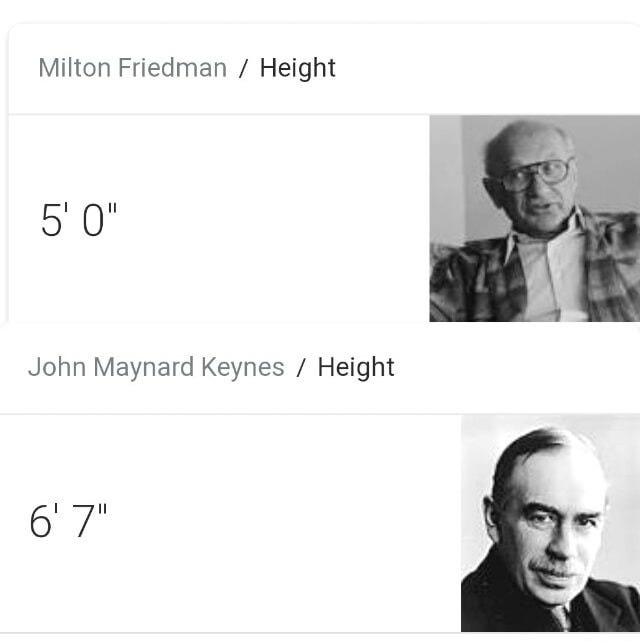

Views about Friedman at the event ranged from being broadly sympathetic, to seeing him as “my life’s vague opponent”. Regardless of what you think of his political views, we should all be able to agree that Milton Friedman led a fascinating life. He made major contributions to microeconomics, macroeconomics, economic history, and statistics,4 and shaped policy across many countries. Despite being so vertically challenged as to almost qualify as a dwarf, Friedman was undoubtedly an intellectual giant.

Even if you know nothing about Milton Friedman, I hope this post will still be interesting. I include a table of contents below, if you would like to navigate to the part that you are most interested in.

Table of contents:

Robin Hanson: Radical mechanism design and the Chicago school

Sebastian Garren: The Chicago Boys and other strange bedfellows

Kadambari Shah: Friedman in India

Readings: Friedman on India.

To prepare for this session, Kadambari told everyone to read a short book, which compiles two sources. The first is ‘Indian Economic Planning’, an essay that Friedman wrote after a two-month visit to India in 1963, at a time when he was studying monetary systems around the world. The second is a memorandum that Friedman wrote for the Indian government in 1955. He visited India that year as part of a delegation from the Eisenhower Administration, which was advising the government of Jawaharlal Nehru, the first prime minister of India, about the Second Five-Year Plan. That delegation was organised by the U.S. International Cooperation Administration, the precursor to USAID.5

The purpose of Friedman’s 1955 visit was to have a more market-leaning force to counterbalance the left-wing economists who had been advising India, many of whom, like Nicholas Kaldor, were members of the Fabian Society. Kaldor – who every economics student knows from his namesake efficiency – advised Nehru on tax policy, and was a major opponent of Friedman’s monetarist views. (We will get to monetarism in section 2.)

We all thought that both of the texts did a pretty good job of diagnosing the problems with the Indian economy at the time. But to understand them, you need to know something about the economic philosophy of India at that time, which Kadambari did a great job of explaining.

The Five-Year Plans

Post-independence India structured its economic development through a series of Five-Year Plans. These were inspired by the five-year plans of the Soviet Union, which, despite many disastrous consequences, did achieve extraordinarily rapid industrialisation. India’s most recent Five-Year Plan didn’t end until 2017. China was similarly inspired to structure its development around Five-Year Plans, which it still does to this day.6

The economic analysis for the Second Five-Year Plan, which covered 1956 to 1961, was based on the Mahalanobis model. Nehru was widely criticised by Western economists for making such high-stakes decisions on the basis of an extremely simplified economic model, which assumed, for example, a closed economy. The export-oriented strategy that allowed the East Asian Tigers to achieve developed-country living standards was never even seriously considered for India.

Skipping over some details about how this model worked, Mahalanobis recommended extremely aggressive investment targets. The Second Five-Year Plan aimed to roughly double the investment-to-GDP ratio. It also recommended that around 60% of investment go to industry, up from 9% in the first plan.

Unless the savings rate increases, investment must be financed by borrowing from other countries. While there were efforts to increase the savings rate among the Indian public, they were nowhere near sufficient.

The new investments were financed through the monetisation of debt: The Reserve Bank of India (India’s equivalent of the Federal Reserve) purchased government bonds directly, which greatly increased the money supply and led to inflation. Debt monetisation is now banned in many countries, precisely because it is seen to create bad incentives for excessive inflation, as in India’s case.7

One of the few pro-market thinkers in India at this time was B.R. Shenoy, who was the sole dissenter on the advisory committee for the Second Five-Year Plan. Shenoy accurately predicted that the Second Five-Year Plan would lead to a spike in inflation, with prices increasing 30% over the course of the plan. This is compared with deflation under the first plan.

It almost goes without saying that Friedman thinks that this entire philosophy of economic policymaking is hocus pocus. P.C. Mahalanobis was a genuinely first-rate statistician: he founded the Indian Statistical Institute, the journal Sankhyā, and was close friends with R.A. Fisher. But when it came to economics, he was hopeless. It’s unclear why a government should target a specific investment-to-GDP ratio, and also unclear what would justify such a massive shift toward industry when agricultural productivity was still so low.8 Friedman writes of Shenoy with great admiration in both essays.

On the flip side, Friedman also writes disparagingly about Harold Laski, the socialist LSE economist who had a major influence on creating the Indian consensus in favour of central planning. Although he never travelled to South Asia, Laski was a mentor to Nehru and to V.K. Krishna Menon.

Beware cultural explanations

For much of the 20th century, India’s economic underperformance was regularly attributed to the legacy of colonialism, cultural factors, or an unfavourable climate. Friedman makes the point that an unfavourable climate could theoretically explain some of India’s underdevelopment in absolute terms, but it can’t explain why its growth had been so disappointing.9 Suppose, for argument’s sake, that due to unfavourable geography, a given country would ultimately stagnate at living standards 20% below those of countries at the technological frontier.10 That, by itself, is not a reason why said country can’t engage in catch-up growth to rapidly reach that (somewhat diminished) frontier. Raj Krishna famously dubbed the persistent failure of India to pluck the low-hanging fruit of catch-up growth “The Hindu rate of growth”.

The book we assigned had a short preface by Deepak Lal, in which he gets quite upset at Friedman for insinuating that the Hindu reverence for the cow is irrational. This is strange, because the original comment was made precisely in the context of Friedman arguing that Indian cultural particularities are not economically important. Agnes Callard pointed out an ambiguity here: there are two ways of reading the cultural critique;

Cultural norms are not significant.

Cultural norms are significant, but they are flexible, and downstream of policy.11

It’s still unclear to me which one of these Friedman believes. Just as Friedman didn’t really engage with race in his analysis of the US, his analysis of India doesn’t incorporate much about culture or caste.

In the session, I was contrasting this with how, in Ireland, people often say that one of the major obstacles to densifying is an Irish cultural attachment to homeownership. I’m inclined to think this is nonsense. For one thing, the Irish homeownership rate is frankly on the low end. For another, extremely strong price signals indicate that people would rather build and move into small apartments at much greater rates than they are currently allowed to. But I’m not sure whether the ‘cultural commitment to homeownership’ is toothless, or whether it is important, but is downstream of land use regulation.

The 1991 reforms

Why start a Friedman event with an India session?

For one thing, I have an inordinate fondness for thinkers who have random side interests in other countries, as with my essay about Keynes in Dublin.12 Tyler’s GOAT chapter about Friedman begins by considering his views on India. But this is idiosyncratic: Friedman’s writings about India are slim pickings. He would not have claimed to be an authority on the Indian economy.

But, more importantly, while Friedman on India is a tiny part of his intellectual influence, it’s a massive part of his practical influence. Maybe even the majority. That is because Friedman was perhaps the strongest international voice against the suite of economic policies adopted after Indian independence, including price controls, hefty tariffs, and restrictions on foreign direct investment. When the Indian government faced a balance of payments crisis in 1991 and had to be bailed out by the International Monetary Fund, economic policy was rapidly reformed under Finance Minister Manmohan Singh in Friedman’s intended direction.

I don’t know how influential Friedman, in particular, was in India. Part of the point of a project that Kadambari works on at the Mercatus Center, the 1991 Project, is to disentangle the influences on that critical moment in modern Indian history.

I will also note that, like everything else in economics, the significance of the 1991 reforms to unlocking India’s subsequent economic success is debated. Ramachandra Guha, in his otherwise masterful history of post-independence India, wrote about it far less than I would have expected. Still, it’s poetic that this model of change aligned so closely with one of Milton Friedman’s most famous quotes:

Only a crisis – actual or perceived – produces real change. When that crisis occurs, the actions that are taken depend on the ideas that are lying around. That, I believe, is our basic function: to develop alternatives to existing policies, to keep them alive and available until the politically impossible becomes the politically inevitable.

I’m with Milton. As an economist wanting to influence policy, you need to have endless patience for repetition, waiting until a crisis. When such a crisis occurs, policymakers reach around for whoever has the most clearly articulated and developed plan in the rough vicinity of what they believe. (I suppose if you’re really unscrupulous, you manufacture the crisis to begin with, as Noam Chomsky would no doubt accuse Friedman of doing.)

The 1991 reforms marked the end of ‘License Raj’ (or Permit Raj). The stated purpose of License Raj was to protect Indian industry and promote self-reliance (swaraj). In practice, it meant that operating a business required navigating a thicket of complicated licenses and regulations, and even honest people needed to rely on bribes and black markets to survive. Indian bureaucracy is still infamous today, as when my own tourist visa there was rejected on five separate occasions for reasons of arcane proceduralism. But I promise, it used to be a lot worse!

The term ‘License Raj’ was coined by Chakravarti Rajagopalachari (‘Rajaji’), one of India’s founding fathers. Among other things, Rajaji led the Swatantra Party, which was one of the only sources of opposition to Jawaharlal Nehru’s Congress Party. Congress has led independent India for most of its existence, and, for most of that time, has been ruled by Nehru’s immediate family. But ironically, the 1991 reforms were themselves implemented by a Congress government.

The whole sequence of events which led up to the reforms was completely insane. Congress’s heir apparent, Rajiv Gandhi, was assassinated by the Tamil Tigers during the 1991 election. That convinced compromise candidate P.V. Narasimha Rao to delay his retirement, and he was rapidly elevated to the premiership. A balance of payments crisis coincidentally happened at almost exactly the same time as the election, and so, coming to power, Rao had immense leverage to implement a radical reform agenda. One of my pieces of advice for developing country governments is: If you’re going to face a major crisis, make sure it’s early in your term.

Although India’s case is not as extreme in either direction as China’s, about three hundred million Indians have escaped extreme poverty since 1991. And if it is indeed the case that the ‘spirit of 91’ is responsible for India’s subsequent decades of solid growth, then it is one of the most important events in modern history. Again, it’s extremely hard to work out how much of this is due to individual thinkers compared with straightforward pragmatism or something else.

A good rule of thumb is that Friedman’s views about almost everything were so cartoonishly extreme that his favoured policies were adopted essentially nowhere, ever. However, at the margin, many policies shifted significantly in his preferred direction during his lifetime. The shift was perhaps most extreme in the case of exchange rate policy. Many emerging markets shifted to freer exchange rate regimes in the 1990s. While the Reserve Bank of India still intervenes to smooth out fluctuations in the value of the rupee, it is much closer to a free market than the previous fixed exchange rate system.13

I was pretty keen to talk to Kadambari about the extent to which India has ever had a tradition of market thought. In The Argumentative Indian, Amartya Sen repeatedly talks about the interfaith dialogues organised by the Mughal Emperor Akbar. He uses them to argue against the Hindutva talking point that secularism is a Western imposition on India. Could something similar be said about an appreciation for the value of markets?

The intellectual father of the 1991 reforms is sometimes said to be the trade theorist Jagdish Bhagwati, who later featured in episode two of Milton Friedman’s TV show.14 If Bhagwati is the father, then Shenoy is the grandfather. But it seems that the number of individuals who kept the flame alive is very small.

In the final part of the session, we discussed Devesh Kapur, who is well-known for highlighting that India has surprisingly high state capacity in ‘big-ticket’ areas (mass vaccination programmes, running elections) while being shockingly bad at providing many lower-level services (clean water, toilets). The 1991 reforms are a perfect example of this: swiftly and successfully executed in a way that set many macro variables on the right track, while proper micro implementation lags to this day. Personally, one of the reasons why I found this session, and India in general, so fascinating is that India’s performance has such a spiky profile for a country at its level of development.

As with most of the things that he writes, I didn’t get much of a sense of how Friedman actually felt about India. Aside from the 1955 and 1963 trips, he visited once more, briefly, in 1979, when filming for his television series Free to Choose. We will get back to that.

Kadambari Shah is a researcher at the Mercatus Center, who also works on The 1991 Project with Shruti Rajagopalan.

Sam Enright: Friedman’s monetary thought in retrospect

Reading: Ben Benanke, On Milton Friedman’s 90th Birthday

Everything reminds Milton of the money supply. Well, everything reminds me of sex, but I keep it out of the paper.

Robert Solow

You couldn’t have a Friedman event without talking about money.

I felt quite underqualified to be covering such a broad and important topic in my session. In preparation, I worked through volumes one and two of Milton Friedman and Economic Policy Debate in the United States: 1932–1972 by Ed Nelson. As the first monetary economist to write such a book, he spends the first chapter grumbling about how previous Friedman biographers have allegedly misunderstood the field.

I ran this session in the same style as my reading groups: By writing up short discussion prompts with questions about topics that I think I would otherwise forget to bring up. You can see all my discussion prompts here.

Before we got to the meat of the session, I reminded everyone that measuring how much money there is is actually extremely complicated. In school, you might have seen money defined as a medium of exchange, a unit of account, and a store of value. But this definition is implicitly relative to a timescale. We all agree that cash is the most unambiguous example of money. But there is a spectrum of how quickly other assets can be converted into cash, and how much of their value they lose in the process of doing so.

Thus, there isn’t really a definition of ‘money’, so much as there is a series of concentric circles which depend on your preference for liquidity. Arguably, if your time scale is unlimited, then anything is money.15 Exactly how the ‘monetary aggregates’ are constructed that quantify these concentric circles is a bit technical for this post, but I’ll put some details in a footnote.16

The Great Depression

In 1963, Milton Friedman and Anna Schwartz published A Monetary History of the United States: 1863–1960. This book presented, for the first time, a continuous monthly and annual time series of the money supply over the previous century. That alone was a monumental achievement, and transformed Friedman into a giant in the field. Despite doing the majority of the empirical work, Schwartz got far less of the credit; Friedman’s frequent coauthorships with women are one of the themes of the Burns biography.

The Monetary History is more famous not for presenting data, but because of its arguments about what caused the Great Depression. Friedman and Schwartz argue in chapter seven that the primary cause of the Great Depression was that the Federal Reserve allowed the money supply to shrink by around a third following an economic downturn in 1929. They failed to act as a lender of last resort, leading to a series of bank failures in the 1930–33 period. This entirely preventable policy error turned what would otherwise have been at worst an ordinary recession into a catastrophic depression. That depression became global through the collapse of the gold standard system, the mechanism of which they also detail at length in the book.17

This was a departure from the previously popular explanations, like that the Great Depression was caused by a stock market crash or an escalating global trade war. Obviously, the Great Depression was caused by lots of things, but Friedman-Schwartz represented a major shift in emphasis – one which has come to be largely accepted by economic historians.

The first thing I said about the Monetary History is that I quite liked the way it was written. The book came long before the credibility revolution or modern causal inference, but it has a lot of focus on careful causal and counterfactual reasoning. As was discussed in the reading, Friedman and Schwartz really only have four historical episodes to analyse. This does not pass econometric muster by today’s standards. Would the most influential book in the history of monetary economics pass peer review today? I digress.

The hero of the Monetary History is Benjamin Strong, who was the Governor of the Federal Reserve Bank of New York. Friedman wrote that “Much of the success during the twenties” could be attributed to Strong.18 During the Strong era, the New York Fed was a particularly influential branch within the Federal Reserve System, and he was personally so widely respected that his views held a lot of sway. Benjamin Strong was a pioneer in the Fed using open market operations (the buying and selling of government securities) to move the interest rate.19 Previously, the main instrument that the Fed had to influence the money supply was the discount rate, which is the rate at which they lend to commercial banks.

Strong had a number of long-term health problems that led to his untimely death in 1928. That unleashed a power struggle between New York and the other branches. New York lost that fight, and the Fed in Washington went back to the old way of doing things. That meant that when there was a series of bank runs in the 1930s, the Fed didn’t provide nearly enough liquidity for the banks to survive.

For this session, the reading I assigned was a speech that Ben Bernanke gave at Friedman’s 90th birthday party. That was in 2002, soon after Bernanke had been appointed to the Board of Governors of the Federal Reserve. The party took place in (drum roll please) the Quad Club, the venue our event was in! However, the sources I read were inconsistent about whether Bernanke’s talk in particular was in that building or in a lecture hall nearby.

I cannot think of any greater way to spend one’s 90th birthday than at an academic conference with all the leading thinkers in your field, where they talk about how right you were all along. The final line of Bernanke’s speech became famous:

Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve. I would like to say to Milton and Anna: Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.

Who were the monetarists?

One of the labels that is sometimes applied to Milton Friedman is ‘monetarist’. It’s a vague term, but one way of thinking about it is that monetarists think that the quantity theory of money equation is extremely important. This equation, MV = PY, is just an accounting identity, which states that the money supply (M) times velocity (V) equals the price level (P) times GDP (Y). However, monetarists believe that velocity is either constant or predictable, which turns this tautology into a useful predictive statement. For example, if the velocity of money is constant, then increasing the money supply by k% will increase nominal GDP (PY) by the same amount.

This is the basis of what is probably Milton Friedman’s most famous quote: “inflation is always and everywhere a monetary phenomenon”. Friedman thought that the MV=PY equation was so important that he had a custom registration plate made of it. You have to admit, this is extremely cool.

The evidence for whether the velocity of money is in fact predictable is mixed. The correlation between inflation and the growth rate of the money supply is much weaker than you might expect in the short run. There are a zillion complicating factors to the idea that “if you just print more money, inflation will go up”. For a good overview of the influence of this tradition, I recommend The Monetarists by George Tavlas.

In my understanding, monetarism is why Friedman was such a strong advocate of gradualism. Friedman’s preferred system of central banking was to replace the discretion of the Federal Reserve with a constant monetary growth rule, in which the money supply should increase by a constant k% per year. The actual value of k is less important than the fact that it stays constant; he suggested 4%.20

The idea is that, even though it is made up of well-intentioned, intelligent people, the Federal Reserve Board is fallible. Part of the point of the Monetary History was to argue that, in effect, a discretionary Fed is a failed experiment; there were fewer financial crises in the period between the Civil War and the creation of the Federal Reserve in 1913 than in the period between then and when Friedman’s book came out. The effusiveness of Friedman and Schwartz’s praise for Benjamin Strong is precisely to make the point that the monetary system relied on having the right individuals in place. And a system that requires having the right individuals in place is a bad system. The Fed, Friedman says, ought to be based on predictable rules.

The irony of this is that, in political culture, the term ‘monetarism’ came to be associated with extremely sudden and unpredictable monetary shocks. If you talk to anyone who remembers political discourse in the 1970s and 80s, they will immediately associate monetarism with the Volcker shock. This was a decision from 1979 to let interest rates rise as high as they needed to go to reduce inflation, which was then in the double digits. This predictably led to a recession in 1981–82.

The Volcker shock was implemented through directly targeting (at least in theory) monetary aggregates. This was a shift away from the previous regime of targeting interest rates and toward the Friedman paradigm. Although he supported the general principle of the Fed controlling inflation through directly targeting the money supply, Friedman thought the execution of the Volcker shock was a mess.

The Fed’s experiment with directly targeting monetary aggregates only lasted about three years. The evidence about the effects of this policy is complicated and mixed.

Friedman had a reputation as an extremist. But, in monetary matters, he was an outlier in how much he favoured predictability and gradualism.

The natural rate of unemployment

In the 1960s, Friedman experienced a meteoric rise as an iconoclast. His first brush with public fame came in 1964, when he served as an advisor to presidential candidate Barry Goldwater. As an eloquent and erudite defender of outrageous ideas, the media loved Friedman.

But in the early 1970s, events began to vindicate Friedman, in a way that made him a figure of mainstream respect. For one, the Bretton Woods system – a quasi-gold standard in which USD was pegged to gold, and all other major currencies had fixed exchange rates to USD – broke down in 1971. Friedman had been predicting this at least as far back as 1953. But his greater vindication was ‘stagflation’, which is a situation where you have both high inflation and high unemployment.

Generally speaking, there is a downward-sloping relationship between inflation and unemployment called the Phillips curve. Between the 1940s and the 1960s, the ascendant framework in economics was Keynesianism. Under Keynesianism, at least as interpreted by Paul Samuelson and Robert Solow, the Phillips curve is a long-run enough relationship that it can be treated as part of a stable menu of policy options.21 Policymakers can decide whether they would prefer to have high inflation and low unemployment, or low inflation and high unemployment, however they see fit.

So under Keynesianism, stagflation is impossible. When it happened anyway, it was so much the worse for Keynesianism. The reason why stagflation could occur is that it turns out the Phillips curve is only a short-run relationship.

In the long run, unemployment is determined by its ‘natural’ rate. The natural rate of unemployment is the rate that would prevail if expectations about inflation were accurate. It is determined by real structural characteristics of the economy: the friction to finding a job, union power, minimum wages, and so on.22

Friedman outlined this view in a famous presidential address to the American Economic Association in 1967. He warned that the expansionary path that the Fed was on would require accelerating inflation in order to continue boosting employment to the same degree. Getting back to normalcy would require a painful adjustment period in which both unemployment and inflation would be high, i.e. stagflation.

If the above explanation didn’t make sense, the best introduction to the history of economic thought I’m aware of is Trevor Chow’s Phoenix Wright: Ace Attorney parody tweet. Friedman coincidentally came up with this idea at a similar time to Edmund Phelps, and the Friedman-Phelps natural rate hypothesis is now widely accepted at least in broad outline.

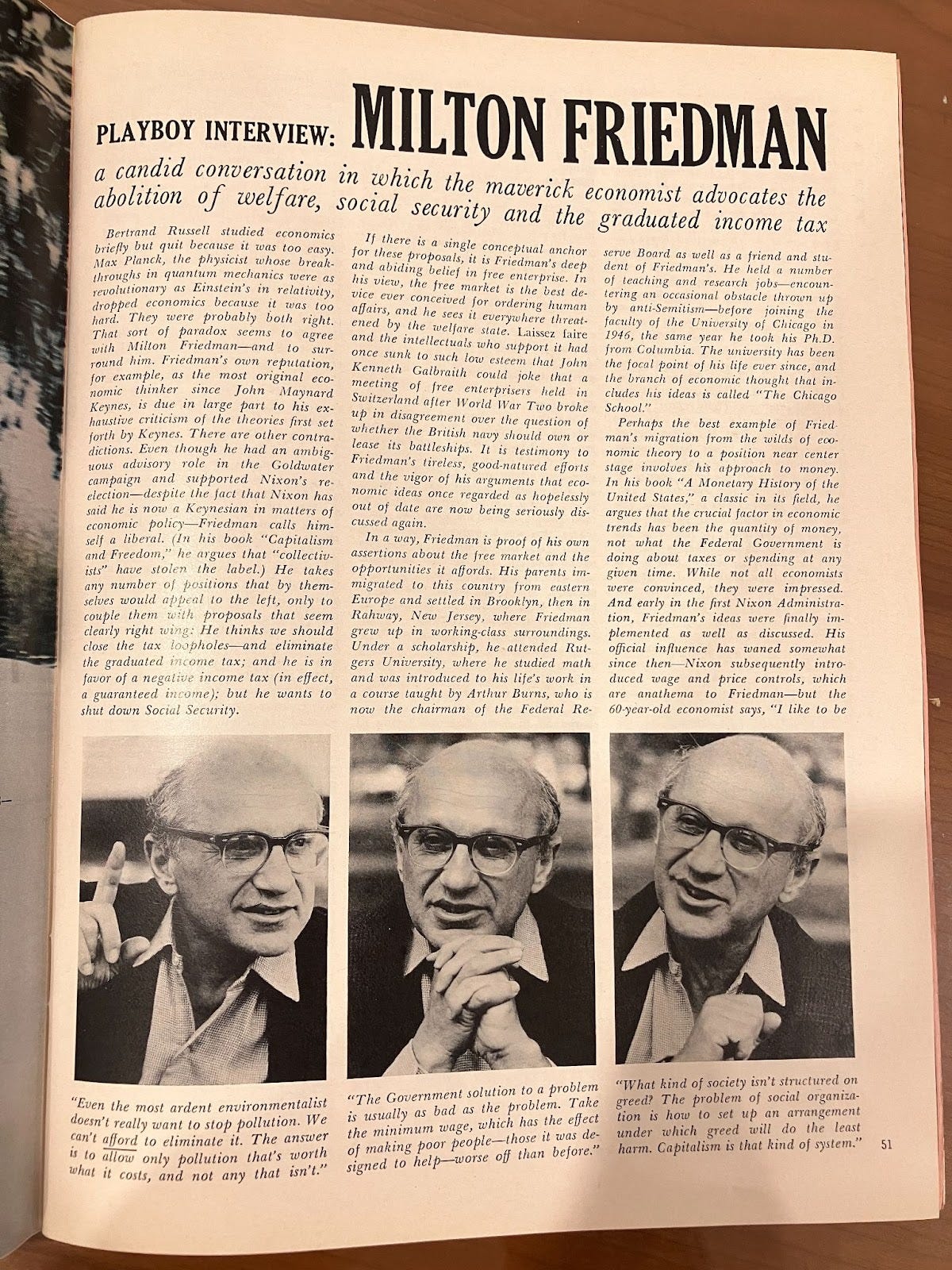

Reading how Friedman responds to these episodes is interesting. I figured that the early 1970s would be a good period to look at from the standpoint of intellectual history. One of the pieces I found from around then was a February 1973 interview about monetarism and other topics that Friedman gave in (of all places) Playboy magazine. It’s surprisingly detailed, and touches on many of the themes from my session.

However, the text of Friedman’s Playboy victory lap was not available online. This may lead you to ask: Did I enter multiple eBay bidding wars in order to track down the right issue for the Friedman profile? Yes, yes I did.

The profile begins by framing Friedman as the most original economic thinker since John Maynard Keynes – and also his intellectual nemesis. It’s one of the most poetic images in the history of economics that Friedman and Keynes were inverses of each other on so many issues. You would not be the first to notice that Keynes, as a British promiscuous aesthete giant, was the exact mirror image of Friedman, an American monogamous philistine dwarf.

Rebecca Lowe: Friedman’s philosophy of freedom

Reading: Capitalism and Freedom, chapters 1 and 2.

I was very pleased when Rebecca Lowe published a blog post about her session at my event. She does a better job explaining her views than I can, so I recommend you go read her post.23 In it, she lays out the groundwork:

In the first chapter of Capitalism and Freedom, Friedman considers which kinds of economic and political arrangements can and do protect and further individual and societal freedom. He begins by stating his opposition to a standard view about the conjunction of freedom and societal arrangements. He describes this standard view as combining the following four claims:

that politics and economics are “separate and largely unconnected”;

that “individual freedom is a political problem and material welfare an economic problem”;

that all political arrangements are compatible with all economic arrangements;

that democratic socialism is an example of this compatibility (e.g., that Russian-type socialist economic arrangements would be compatible with American-type democratic arrangements).

So the standard view, as Friedman presents it, consists of two big claims (1 and 3), and two respective examples (2 and 4).

Friedman focuses on the two big claims, and claims instead:

that there’s an “intimate connection between economics and politics”;

that some combinations of political arrangements and economic arrangements are not “possible” (and indeed that democratic socialism is an example of an incompatible combination, at least if democracy involves “guaranteeing individual freedom”).

The rest of the chapter is aimed at persuading us of the superiority of the Friedman view.

My first question to the group was: Does anyone really believe the ‘standard view’? Perhaps it was more common in the 1960s, when under Khrushchev the Soviet Union was beginning to allow greater political freedoms, and history had not ended yet so decisively in favour of liberal democracy. But to me, it seems self-evident that your choice of economic system has implications for your political system, at least on average. ¯\_(ツ)_/¯

In the reading, Friedman also has a ‘historical’ section, for which his main conclusion is that capitalism is a necessary but not a sufficient condition for political freedom. Rebecca gives various arguments against Friedman, which I would again encourage you to read.

A representative passage from the early sections in Capitalism and Freedom will have Friedman argue that socialism doesn’t leave room for political dissent in the way that capitalism does. It is true enough that many (most? all?) attempts at socialism have involved unacceptable restrictions on dissent. But what to make of the idea that, under capitalism, there will be such large accumulations of wealth that (say) billionaires can fund think tanks and media organisations to parrot their positions, or that businesses can bankroll political campaigns which favour their special interests? I am somewhat less concerned than many people are about the alleged role of money in politics, but this is because of a contingent body of empirical evidence and arguments from political science. I certainly don’t think that such concerns can be dismissed out of hand. But Friedman just doesn’t engage with serious arguments for why capitalism might stifle dissent.

I don’t think you can understand why Friedman loves freedom so much without understanding that he thinks that the universe has an entropic force that pushes toward tyranny. In the long arc of human existence, freedom has been extremely rare. Most of the time, it never really had the chance to get off the ground. In some cases, it has collapsed due to malice and power-seeking. But in the most tragically ironic cases, respectable, well-intentioned people have voted away their freedoms. Friedman had no problem with people living in the kibbutz, or other entirely voluntary forms of collectivist living that restrict freedom. The trouble is in not having those voluntary restrictions on freedom spill over and influence the rest of us.

Striking and suspicious convergence

My first opinion about this is that Capitalism and Freedom is a very vibes-based book. I am sceptical that a priori philosophical theorising can get us very far here. Friedman doesn’t hold himself to the standards of analytic philosophy, despite writing as though he’s trying to.

Before coming to a firm view on the topic, I would want to engage substantively with the empirical literature from political science on the relationship between political and economic freedom. If it turns out that literature is crap, then we can fall back on vibes. But Friedman doesn’t seem to think this is necessary.

My second opinion echoes Stefan Schubert’s argument that multiple-factor explanations should not appear one-sided. It’s common in academic writing for an author to give a long list of reasons why some phenomenon was likely to occur. But, for a complicated chain of causation in which approximately everything is correlated with everything else, then at least some of the factors should make the phenomenon less likely, even if on net it was still made very likely. Schubert takes aim at science popularisers like Jared Diamond, who will purport to be “explaining” something like why agriculture first arose in the Fertile Crescent. Diamond does not mention any reasons why agriculture might have been less likely to arise in the Fertile Crescent, even though such reasons almost certainly exist. This makes it hard to tell when someone is just cherry-picking.

In Friedman’s books, we hear lots of reasons why largely unfettered capitalism makes X more likely, where X is some desirable goal. But we don’t hear a peep about the ways in which capitalism makes X less likely. I frequently agree with him that, on net, capitalism promotes X. But the key word is ‘net’. Realistically, the world is extremely complicated, and market mechanisms can both promote and inhibit various goals.

Economic theory has its place, but, to paraphrase Matthew 4:4, man shall not live by vibes alone. I think that you do often just need to be familiar with lots of contingent empirical details to thoughtfully opine on how important different factors are. This is related to my feeling that memorisation has been systematically undervalued in education, and that ‘just knowing a lot of things’ is an underrated characteristic of intellectuals.

Friedman was an extremist, not just in the libertarian philosophy where he landed, but also in thinking that all roads lead to Rome; every consideration and argumentative strategy seems to lead us to the same conclusion. Even when I agree with where Friedman ends up, I don’t necessarily agree with how he got there.

We were talking about this striking and suspicious convergence with Ben Conroy, a philosophy PhD student at the University of Chicago. One explanation is that Friedman is a biased ideologue.24 But an alternative hypothesis, which logically would explain his views equally well, is that Friedman is just correct. In this case, it would just be that “reality has a well-known libertarian bias”. I leave the details of this as an exercise to the reader.

Efficiency versus equity

In economics, you’ll hear a lot about the equity-efficiency tradeoff. Intuitively, there are many cases in which helping resources be directed to their highest-value use (as measured by willingness-to-pay) will make particular groups worse off. Compared to philosophers, economists are incredibly vague about what they mean by the word ‘equity’. I take it to mean any goals we have about making the distribution of welfare more equal, separate from the absolute amount.

Essentially all of Friedman’s economic analysis is about cases where equity and efficiency happen to move in the same direction. For example, ‘Roofs or Ceilings?’ is a famous (ok, ok, “famous”) pamphlet he wrote with George Stigler, in which he argues that rent controls are bad for both equity and efficiency.

At some level, I agree that most people greatly overrate the equity-efficiency tradeoff. The benefits from the extra efficiency are frequently so large that the worse-off groups are small, if they even exist at all. There is some debate over what exactly Adam Smith meant by his ‘invisible hand’ metaphor, but at least one of its uses seems to me to be saying that equity and efficiency move together surprisingly often.

At the end of each episode of Free to Choose, there is a panel discussion, in which a group of distinguished guests debate with Milton Friedman in Harper Library at the University of Chicago. In episode five, his critics are probing into the tension between equity and efficiency. Even if we disagree about how often it occurs, it’s impossible to deny that there are some cases where equity and efficiency come into conflict; such cases seem like a worthy target for government redistribution. What to do then?

To Friedman, efficiency is almost synonymous with economic freedom. Freedom is fantastic at maximising the total amount of economic welfare. On the panel, Friedman’s critics eventually get him to admit that, if freedom led to increased inequality, then he would still favour increasing freedom. But he speaks of that as if it were a far-fetched hypothetical.25 They probe more about what to do in cases where you have to choose between freedom and equality, and he repeatedly dodges the question. He gets increasingly flustered, and eventually says “You can only serve one God”.

This was a funny quip. But as an actual philosophical position, it is completely stupid. Even Robin Hanson, the biggest contrarian in a room full of contrarians, was unable to defend it.

The idea that Friedman is philosophically naïve is perhaps the dominant view among the general public. Many people believe this, in that they believe Friedman was an absurd caricature who thought greed was somehow good, or that we should be unconcerned about helping the poor.

I sometimes joke with my friends that the worst people in the world are people who agree with you, but for different reasons. I think that Friedman’s philosophy is weak for reasons that are basically unrelated to popular perceptions about him. I had never really seen these weaknesses explored before, which is one of the reasons why I found this session (and event) valuable.

Rebecca Lowe is Philosophy Senior Research Fellow at the Mercatus Center. You can read her Substack here or follow her on Twitter here. She is writing a book about what ‘freedom’ would mean in utopia.

Robin Hanson: Radical mechanism design and the Chicago school

Reading: Free to Choose: A Personal Statement, chapters 4 and 6.

Free to Choose: A Personal Statement, which Milton Friedman coauthored with his wife Rose (née Director), was the book adaptation of his TV series. From it, Robin assigned chapter four (social welfare) and chapter six (education). Conveniently, the chapters in the book have the same numbering as the episodes, so you can also follow along by watching episode four (‘Cradle to Grave’) and episode six (‘What’s Wrong with Our Schools?’). Friedman used to say that Capitalism and Freedom was “The Old Testament” and Free to Choose was “The New Testament”.26 Together, they give you a broad overview of his worldview.

We had a good chuckle about the fact that Free to Choose is more intellectual than almost any TV show I can think, and that it aired on PBS, a publicly-funded broadcaster. Of course, media production is dominated by the private sector, and there simply was not much market demand to produce more of this kind of content. As Robin put it, the people voted, and “the people wanted slop”.

The negative income tax

Friedman was an advocate of abolishing the welfare system. The arguments against it are well known: welfare produces a perverse incentive for society’s poorest to avoid working, since they typically lose access to benefits after doing so. The purveyors of welfare also impose paternalistic conditions on their support, which (it is argued) keep people trapped in a cycle of poverty. When welfare is distributed through in-kind benefits, like social housing, it concentrates the most vulnerable members of society into a confined area, increasing crime and other social issues.

Free to Choose also claims that one of the worst features of the welfare system is that it led to a collapse in support of private charity. He claims that rates of charitable giving in the 19th century were much higher than they were in the 20th. I suspected that this would be another empirically dubious Friedmanism, but the 19th century really was a remarkable era of charity. Before the government was expected to be such a gigantic force in our lives, many of its social protections were provided through religious associations, friendly societies, and other mutual aid organisations.

Friedman’s signature proposal to replace welfare was the negative income tax (NIT). It works like this: the government provides a minimum income for all citizens, even if they don’t work. When you start to earn money, your income tax is paid at first in the form of deductions from the minimum income allowance. This is done in such a way that, at every income level, people have a constant incentive to continue working – a far cry from the highly non-linear and confusing incentives you face under a graduated system. Eventually, you’ll reach a breakeven point where the government is neither subsidising nor taxing you. Past that, you will finance the ‘negative tax’ for poorer people.

This is why people sometimes say that Milton Friedman was a supporter of a universal basic income. You can design a negative income tax whose payouts are mathematically identical to any given UBI. But, arguably, they are quite psychologically different. Under a negative income tax, the government only sends out cheques to people who are below the break-even point. Under a universal basic income, the government conspicuously sends out cheques to everybody, and its uniformity is one of the arguments most favoured by its proponents.

The way that he talks about it in the TV episode is that negative income tax would be a temporary measure, in order to phase out our current welfare system. But in the book version, he vaguely makes it sound like some amount of negative income tax would still exist in utopia. He clearly thinks that, if we had more economic freedom, the number of individuals who are so destitute as to need governmental assistance would be much reduced. But we genuinely couldn’t figure out whether Friedman thought of NIT as a temporary or permanent measure.

In a panel discussion, Friedman also predicted that, since welfare contains the “seeds of its own destruction”, the introduction of NIT was inevitable. To me, this seems like a bad prediction.

Welfare is one of the areas in which Friedman had the largest concrete policy influence. Richard Nixon attempted to pass a negative income tax in the form of the Family Assistance Plan (FAP) in 1969. There were enough exemptions from a ‘pure’ NIT that Friedman ended up testifying in Congress against it. FAP passed the House but died in the Senate, killed by a strange coalition of rightists concerned that it was too generous and leftists concerned it wasn’t generous enough.

It’s quite remarkable how close the United States came to having (a form of) universal basic income, largely because of Milton Friedman. Negative income tax also influenced the design of the earned income tax credit, which came into effect in 1975. While the EITC has some characteristics in common, real negative income tax has never been tried.

Many of the problems that Friedman describes (inner city ghettos, long-term dependency on welfare) were indeed very bad in the 1970s and 80s. He takes this as a sign that the whole system is inevitably going to collapse. But instead… things got much better. The crime rate fell dramatically. Poverty went down. Welfare was reformed to exclude long-term reliance, and, empirically, welfare fraud is rare.27 I don’t think we fully understand why so many American social indicators started trending in the right direction after the publication of Free to Choose, but I think that the verdict on welfare ended up being less dystopian than what they outline.

School vouchers

Friedman was also an advocate of abolishing public schools. Public schools are a monopoly: they are insulated from competitive pressure to deliver a high-quality “product”. It’s unclear why the government would have a comparative advantage in being the organisation to do the day-to-day running of education, and why the goals of public education can’t be achieved in other ways.

Friedman’s signature proposal for education policy is school vouchers: publicly-funded vouchers redeemable against the tuition at any school the parents choose. His advocacy for this was also very influential, helping to birth the school choice movement. Under school vouchers, the state funds education, but doesn’t provide it directly. Schools, if you like, are ‘contractors’ to provide education.

It bothers me when people act as if the answer is obvious about whether various state-subsidised goods should be provided directly by the government, or through contractors. This is the subject of one of my favourite economics papers, by Andrei Shleifer.

A close historical analogy to school vouchers is the G.I. Bill, the legislation which financed many returning veterans from the Second World War to attend higher education. Interestingly, the G.I. Bill allowed veterans to spend their vouchers at religious and other private universities.

What came next in the discussion was us suggesting a series of reasons why the state should provide education directly, and Robin telling us why we were wrong.28

Maybe the purpose of public schooling is to instil common civic knowledge and responsibility in future voters? This is difficult to square with the fact that most voters are extremely unsophisticated, and don’t even understand the basic functioning of government. Public schools might also be more propagandistic than private ones.

Maybe some parents cannot be trusted with decisions about their children’s education? There may be something to that. But why be confident that the government is so much more trustworthy? Perhaps I’ll write about this some other time, but I believe my own public education actively pushed harmful and ineffective pedagogy.29 Educational psychology is in a poor state; insofar as we do know how to teach well, I don’t see indications that this knowledge is consigned to specially trained and government-certified educators.

Maybe the purpose of public education is just to ensure that the entire population is up to a minimum standard of literacy and numeracy? The Friedmans’ position shifted on whether this means that a school voucher system needs to be supplemented by compulsory attendance laws. In Capitalism and Freedom, Friedman says that all children should be legally required to go to school, because literacy has such large positive externalities.30

But in Free to Choose, the Friedmans say they’ve changed their mind. As I understand it, their claim is that compulsory schooling laws are unnecessary, because the free market already achieved near-universal levels of literacy before compulsory attendance laws existed.31

They largely rely on statistics from Massachusetts. But as we know, New England Puritan settlers were sociologically extremely unusual. Taking people called Ezekiel with fourteen siblings who learned to speak Ancient Greek before the age of five as the comparator group for what would happen in a free market in education is out of line from Ole’ Milton.32 Also, whenever you see a statistic about how the rate of school attendance was surprisingly high in the 19th century, this is misleading, because the school year was a lot shorter (as were the individual days). Here is GPT-5 contra the Friedmans.

There is a tradition of pro-market thinkers arguing that compulsory schooling laws were not nearly as effective as you might expect in raising literacy, numeracy, or educational attainment. The Friedmans are not claiming that the laws had no effect – just that a sufficient level of literacy to sustain a free and democratic society was achievable without them.

There is, of course, much to be said about all of this. Particularly spirited in this session was the economist Muireann Lynch. She also brought her fourth child, a sixteen-month-old, who was a big hit. I have faith that Muireann will eventually start a Substack and fulfil her destiny of becoming Irish Emily Oster.

Some of the disagreement between Muireann and others centred around whether the state has an obligation to provide a good, even if we somehow knew that all or almost all the same people would still receive that good under a free-market system.33 There does seem to be something virtuous about the state providing a guarantee of education, even if only a small number of individuals would make use of it.

I often wonder about how much time we should all be spending in discussions that feel like they are bottoming out in intractable differences in intuition. This was one such discussion. Agnes Callard once told me that the conversations that are most socially difficult can be the most intellectually fruitful. I suspect I’m a wee bit hasty to move on from topics if it doesn’t feel like we’re getting anywhere.

Finally, Robin summarised all of Friedman’s arguments about social policy in the following way:

Where’s the beef?34

Where is the actual argument for why there needs to be a welfare bureaucracy, instead of a guaranteed minimum living standard? Where is the actual argument for why the state needs to control education? To those of the Friedmanite persuasion, we can achieve acceptable living and educational standards without government control. And, if we don’t need it, why should we have it?

Robin Hanson is a professor of economics at George Mason University who writes Overcoming Bias. You can follow him on Twitter here.

Agnes Callard: Milton Friedman as a public philosopher

Readings: The Social Responsibility of Business Is to Increase Its Profits, Milton Friedman on the Phil Donahue Show

I was first made aware of Agnes Callard by a three-hour shockingly entertaining philosophy seminar that she ran with her ex-husband Ben on “the philosophy of divorce”.35 It turns out that one of the topics over which she can bond with Ben is a mutual interest in Milton Friedman.

The first assigned reading for this session was probably Friedman’s most infamous essay, a New York Times editorial from 1970 in which he argues that the only ‘social responsibility’ that businesses have is to maximise profit. The piece is often cited as the apex of greed, neoliberalism, and anti-government demagoguery.

The opening lines of the editorial are legendary:

WHEN I hear businessmen speak eloquently about the “social responsibilities of business in a free‐enterprise system,” I am reminded of the wonderful line about the Frenchman who discovered at, the age of 70 that he had been speaking prose all his life.36

Friedman’s position seems to be that a corporation having any goals other than profit-maximisation is actively unethical. Now, there are certainly lots of reasons to be sceptical of corporate social responsibility. Sometimes, companies fund nonprofits that are engaged in political activities that benefit their industry (disguised lobbying). Other times, they do it to deflect attention away from their immoral or illegal behaviour. I think it’s also fair to say that excessive engagement by corporations in social causes has had negative externalities (the dreaded ‘woke capitalism’).

But still, if a company chooses to donate 10% of its profits to GiveWell, then I think that is fantastic. Quite likely, they will get outcompeted by a less ethical company, so it may not be sustainable. But Friedman seems to think that even this would be actively bad. How?

Much of this session consisted of us trying to reconstruct Friedman’s argument. But ultimately, I do think that it’s muddled. It’s not clear to me whether Friedman knows what Friedman is saying. There is evidence that he wasn’t happy with how the piece turned out.

Here is one attempt: Society is based on contracts, and you have a moral responsibility to uphold contracts. There may also be a ‘social contract’ or other contracts you have agreed to implicitly, but we won’t go there. Corporate social responsibility violates the contracts the business has both with the employee and with the shareholders, both in spirit and (if it were actually enforced) in the letter of the law.

Suppose I’m working for a startup that paid me largely in stock. I signed up on the assumption that the CEO would maximise my returns to the best of his or her abilities. Even something that sounds benign, like funding carbon offsets for the company’s activities, is violating the spirit of what we agreed to.

Why then, can’t we just have more specific contracts? Why not have an employment contract in which your employer will do their best to maximise profit, only after their carbon offsets? My sense is that employment contracts rarely have these kinds of specific carve-outs for corporate social responsibility. One of the challenges of the modern workplace is navigating that my employer may sacrifice an unknown amount of profitability to support social causes I may or may not agree with.

There are some interesting legal issues at play here. Fortunately, Anup Malani, who is a professor at the UChicago Law School, was able to explain a lot to us. There is a widespread urban legend that a board of a company has a legal responsibility to maximise shareholder value; some people even think that Friedman’s essay is partly responsible for this belief.37 In principle, the board can do whatever it wants, including firing the CEO for any reason. It’s common for shareholders to bring lawsuits against the board, but these need to be framed in terms of alleged fraud or negligence, not that the company generated insufficient returns.

What’s interesting is that, since the 1970s, the court system has been increasingly generous to the board and executives about how much charity and social responsibility they are allowed to engage in before it is considered negligent. If you sue the board of a company you own shares in because the CEO is squandering away all your profits donating to PlayPumps International, you are extremely unlikely to win. But, to the best of my knowledge, the underlying law (at least in America) hasn’t really changed.

I think it’s reasonable to be annoyed about this: companies play a very specific role in society and the legal system. Charities also play an important role. But in practice, we’ve been exploiting a legal ambiguity to partially outsource (particularly low-quality?) charity to corporations.

One of the difficulties is that it’s often unfalsifiable whether corporate social responsibility was actually profit-maximising after all. Signalling your allegiance to various charitable ventures might attract new customers, or employees who are willing to be paid less through a compensating differential. So I would expect the law surrounding corporate social responsibility to remain ambiguous.

Agnes’s eventual conclusion was that Friedman is burying an implicit normative judgement in this piece. Without admitting to it, he regards it as a virtue to “stand up for business itself”. Another moral intuition that kicks in for him is his hatred of the idea of spending other people’s money. When the CEO decides to forgo profit for social goals, he is not making an admirable personal sacrifice; he is making a decision on the shareholders’ behalf. That has the same issues as using taxation to support charitable causes. The fact that the cause is worthy is almost beside the point.

The case against Friedman’s “other people’s money” argument is that corporate social responsibility is priced in. If we say that a business is engaged in charity to the extent that it voluntarily forgoes some of its profitability, that should result in lower stock prices. The shareholders thus implicitly agree to corporate social responsibility, insofar as they bought the stock for a lower price than they otherwise could have. I’m not sure what Friedman would say in response to this.38

Friedman versus Smith

There are some peculiar turns of phrase in the NYT essay. Friedman says that businesses have a moral obligation to maximise profit “while conforming to the basic rules of society”. What are the basic rules of society? Doesn’t this just shift the buck, where corporate social responsibility is justified not by the particular relationship between the company and the shareholders, but between the company and society?

However, the remark we spent longer trying to understand was Friedman’s use of Adam Smith’s quote in The Wealth of Nations that “I have never known much good done by those who affected to trade for the publick good”. The original context of the quote is extremely specific: he’s talking about merchants lobbying for trade restrictions, while claiming that such restrictions benefit the national interest. It’s not some kind of general argument against corporate social responsibility, which is how Friedman seems to be quoting him.

Friedman studied Smith closely, and certainly knew the original context of the quote. Is he trolling? Is he saying that all attempts at ‘trading’ for the public benefit are ‘affected’, i.e. insincere? Is he saying that even sincere attempts to trade for the public good are bound to be counterproductive? We couldn’t quite figure it out.

In fact, one of Agnes’s most valuable contributions was in comparing Friedman to Smith. Adam Smith is an incomparably deeper and more sophisticated thinker. I’m not sure I can easily explain exactly how, without just encouraging you to read his original works and the write-up of my Smith conference. Smith manages the rare feat of being incredibly highly rated while still being underrated. I could believe that he is the GOAT.

The Modigliani-Miller theorem

In the next part of the session, we thought about corporate social responsibility in the context of a ‘market for altruism’. Anup happens to have a great paper on this topic from 2009.39

For background, he had to explain to us the Modigliani-Miller theorem. Stick with me here.

The Modigliani-Miller theorem says that the total valuation of a company doesn’t depend on the particular split between debt and equity financing. The basic intuition is that if a company leverages up (takes on more debt), the equity becomes riskier, because debtholders get paid first when the company makes money. But, in an efficient market, the expected return to equity holders increases to compensate for that extra risk. The two effects exactly offset, so the weighted average cost of capital doesn’t change. And the weighted average cost of capital is the rate at which future cash flows are discounted in the calculation of a firm’s value. Thus, the value of the company stays the same.

The Modigliani-Miller theorem rests on some strong assumptions; like most economic theory, the focus is on how reality differs and why.40

By Cowen’s second law, there is a literature about how to explain corporate social responsibility through the Modigliani-Miller theorem.

The basic idea is that investors get utility from two sources: personal consumption and a charitable “warm glow”. When you buy stock in a company that does corporate social responsibility, you are purchasing a bundle good: part financial investment and part charitable donation.

One paper about this proves that, if individuals view corporations and non-profits as equally competent suppliers of “warm glow”, then a change in a firm’s social policy will induce exactly offsetting changes in individuals’ personal donation decisions. Just as there is no effect on firm valuations by leveraging, there is no change in the aggregate supply of “good works” by corporate social responsibility. Capital structure is irrelevant because investors can choose how leveraged to be, and the “philanthropy structure” of a firm is irrelevant because the shareholders can do their own giving.

This analysis is considerably more sophisticated (dare one say more Chicagoan?) than Friedman’s original essay. And it might be completely the wrong model of why people support corporate social responsibility. It could instead be a commitment mechanism. I might find it difficult to build up the willpower to donate 5% of my income to charity every year. It may be psychologically easier for me to instead take a job in a more socially conscious company, that pays 95% of the wage.

The final comment I made about this was that, if Friedman were alive today, it would be interesting to hear his thoughts about the effective altruism movement. Many clever young people at some point get sucked into the libertarian blogosphere, when they have an epiphany amounting at some level to “the government sucks”. Many of those same people later get sucked into the effective altruism blogosphere, when they have an epiphany that “charity sucks too”.

The “government sucks” crowd make some good points, but, to my mind, they also have an unjustified faith in the efficacy of private charity. Not once did I come across a hint in Friedman’s writing that the charities that would supposedly spring up to provide services to the poor if his favoured policies were chosen might suffer from many of the same institutional problems as governments themselves.

Friedman’s public image

In Agnes’s session, we mostly focused on the NYT article, but the Phil Donahue interview she assigned is a gem. Friedman was absurdly quick on his feet, and talented at dealing with the media. Free market principles have never had such an eloquent defender on video and radio. He’s also a fine writer, if a bit plain.

In the Donahue clip, Friedman is always smiling and impeccably polite. In many of the Free to Choose clips, he’s funny and has the audience in the palm of his hand.

It’s hard to imagine any economics professor being as famous today as Milton Friedman was. Free to Choose was the #1 bestselling book in America. The TV show received millions of viewers per episode. The reason why I asked Agnes to run this session is because of her experience with and reflections upon public philosophy. If you want to understand ‘public economics’, you must understand Milton Friedman.

Agnes Callard is a professor of philosophy at the University of Chicago and the author of Open Socrates: The Case for a Philosophical Life. You can follow her on Twitter here or read her Substack here.

Sebastian Garren: The Chicago Boys and other strange bedfellows

Reading: Notes on the Drama of Chilean Economic History

When we decided to host an event about Milton Friedman, one of the topics I wanted to cover was Friedman’s alleged influence on Augusto Pinochet’s regime in Chile. This is one of the most infamous things about him, and is a reason why he was often protested or even physically threatened in the latter part of his career. His acceptance of the Nobel Prize was also interrupted by protesters of Pinochet.

I am indebted to Sebastian for reading up on this topic in so much detail in order to present it to the group. He went above and beyond, and wrote up an excellent blog post recounting the economic history of Chile in preparation for the event. Sebastian also very kindly wrote about the Friedman conference in his annual letter. As a polyglot who teaches Latin and Greek to the students at his middle school in St Louis, Missouri – now enrolling! – Sebastian even brushed up on his Spanish for the purposes of our conference.

Sebastian started the session by asking us: Who are the dictators that are so bad that you wouldn’t advise them? If Xi Jinping offered you a job as his economic advisor, would you take it? What about Putin? Kim Jong-un? If Western academics entirely refuse to steer objectionable regimes in a better direction, won’t they get even worse? Who is helped by that?

On the other hand, won’t prestigious Westerners advising for a regime legitimise their cruelty and despotism? Is this, in fact, what Friedman did for Chile?

Pinochet’s coup

Everything I know about Chile’s coup d’état on September 11th 1973 comes from the Rest is History podcast series about it. In their account, it’s inaccurate to say that the CIA supported the coup. They had no idea it was going to happen. It’s true that the CIA supported “coup-like conditions”, as they did in many places. But Augusto Pinochet was widely regarded as a loyalist to Salvador Allende, the Marxist president who had been elected in 1970. There was a previous coup against Allende that Pinochet had been responsible for stopping, and as such, the CIA believed that Pinochet would actually thwart any coup they attempted. Pinochet was persuaded to participate in the coup only a few days before it happened, but quickly discovered that his personality was well-suited to being a dictator.

In a small detail which is revealing of the lack of attention people pay to recounting this story, almost everyone pronounces Pinochet’s name incorrectly: the ‘t’ is not silent!

The culture of the Allende regime was bizarre and fascinating. Allende’s promise of a Republic of “endless wine and empanadas”, along with a compliant central bank, resulted in annual inflation of over 500%. The finance minister, Fernando Flores, launched Project Cybersyn, an attempt to apply cybernetics to centrally plan the economy on a handful of IBM mainframes.41

In none of the critiques of Friedman’s alleged role in Chilean economic history did I see it mentioned that what Pinochet was replacing was a largely forgotten techno-utopian mathematised vision of communism. Flores’s cybernetic methods were cut from the same cloth as Leonid Kantorovich’s linear programming methods, which had led to a measure of success in calculating more sensible production targets in the Soviet Union. You have no idea how much I want someone to write a Latin American version of the novel Red Plenty about this.

After the coup, Flores was imprisoned by Pinochet’s military junta. When he was released three years later, he enrolled in a PhD in the philosophy of language from Berkeley under John Searle. He then co-authored an influential trade book about symbolic AI with the namesake of one of the most historically important tests of language model reasoning, before becoming a Chilean politician again. And he’s still alive! In retrospect, I wish I had invited him to our event.

The Chicago Boys

Sebastian told us that essentially everything that is commonly believed about Friedman’s influence on Chile is completely false. When I hear people bring up this example, they are usually not interested in the details of Latin American history. Rather, the story is used to score ideological points in one direction or another, typically aligning with some American culture war.

There is a garbled version of the story of Friedman’s role in Chile, which goes something like this:

The CIA funded a coup against Chile’s democratically elected socialist president in 1973. They (the CIA? The Nixon Administration? UChicago faculty? It’s never quite clear…) then dispatched a cadre of economic advisors – the ‘The Chicago Boys’ – who had been taught by Milton Friedman to set the economic policies for Pinochet. The Chicago Boys imposed unfettered capitalism/neoliberalism/the Washington Consensus on the people of Chile. Poverty, inequality, and violence resulted.

There are equally garbled right-wing versions of the story, but we will get to that…

The name ‘Chicago Boys’ makes it sound like Chile’s economic reforms were written or imposed by Americans. But love or hate the economic reforms of the Pinochet regime, they were implemented entirely by Chileans. The Chicago Boys were a group of around 25 to 30 young Chilean economists led by Sergio de Castro. They had been undergraduates at the Pontifical Catholic University of Chile, who then received graduate training in economics at the University of Chicago under an exchange programme. The exchange was organised by the International Cooperation Administration (the precursor to USAID), and largely funded by the Ford and Rockefeller Foundations.

Ironically, Friedman was not even the most influential economics professor at the University of Chicago on this group. That title undoubtedly goes to Arnold Harberger. Harberger personally mentored many of the Chicago Boys, heavily promoted the exchange programme, and even married a Chilean. Yet few people outside economics have even heard of Harberger.

As a general rule, if inflation in your socialist Latin American country is 500%, and Henry Kissinger is whispering in the ear of Richard Nixon, the writing is on the wall that your days in power are numbered. As such, in December 1972, some old navy hands commissioned a group of economists to write a plan for how the military should manage the economy if they decided to take over.

In response, de Castro and his boys wrote El Ladrillo (‘The Brick’), a monograph which provided a roadmap for market reform.42 It recommended the elimination of price controls and tariffs, a floating exchange rate, and the establishment of central bank independence. The Chicago Boys unsuccessfully tried to get the conservative opposition to Allende to adopt El Ladrillo.

After Pinochet’s coup, the military junta immediately devolved into factional infighting. Much of the leadership was strongly opposed to privatisation and to ending price controls.

That is where Friedman enters. He visited Santiago in 1975, during which he gave some talks to businesspeople and military officers. The visit was organised by Rolf Lüders, who was the only Chicago Boy with whom he had a personal relationship. Friedman and Harberger also met Augusto Pinochet for 45 minutes – a visit that would haunt him for the rest of his life.

Soon after, Pinochet decided to put the Chicago Boys in charge of running the economy, and appointed de Castro as Finance Minister.

The McKinsey theory of change

Friedman’s visit seems to have been just the push that Pinochet needed to put the Chicago Boys in charge of running the economy. Sebastian’s blog post is filled with bangers, and I strongly recommend reading the whole thing:

Like a CEO who wants to change the org chart and operational structure but first wants someone from McKinsey to tell him to do it, Pinochet and his military apparatus needed the little push from this famous outsider to hand over the keys to economic reform to Sergio de Castro and his American educated colleagues.

There are differing views about whether Friedman really was so important. Tyler Cowen agrees with Sebastian’s assessment.

At the event, we took to calling this general theory of the way that prestigious Westerners can have influence ‘the McKinsey theory’. The McKinsey theory is related but distinct from the crisis theory of political change we discussed in the India session. A prestigious outsider can break the deadlock between rival factions within an organisation.

As for whether Chile’s economic reforms were a success, that’s a complicated story. Noah Smith has a post arguing that Pinochet’s economic policy is vastly overrated. The record of economic performance under the dictatorship is poor. Chile has been relatively successful since the transition to democracy in 1990, but this can arguably be mostly explained by a copper-exporting boom.

Friedman made one further visit to Chile, for a meeting in 1981 of the Mont Pelerin Society, a group of free-market intellectuals. During that time, Chile was going through a severe currency and banking crisis as a result of an overvalued exchange rate. The economic woes of the early 1980s are often blamed on Friedmanite economics, but I don’t buy it. Despite earlier writing papers in favour of a free-floating rate, Sergio de Castro, for unclear reasons, hard pegged the peso to the dollar in 1979. Friedman, of course, strongly opposed this, and criticised de Castro in his memoir.

The first book to really get all the details of this story right is The Chile Project: The Story of the Chicago Boys and the Downfall of Neoliberalism by Sebastián Edwards. Edwards is a Chilean who studied at the University of Chicago, is close friends with Harberger, and was persecuted under the Pinochet regime. His credentials are impeccable. Edward’s book goes into detail about how much the Chicago Boys were aware of or participated in the tyranny of the regime. One argument against is that the head of the secret police, who was responsible for thousands of extrajudicial executions, was gathering intelligence on the Chicago Boys and was clearly looking for any excuse to kill them.

The legacy of the Chicago Boys is being debated once again in Chile. The current president-elect of Chile is the right-wing José Antonio Kast, who won the 2025 election against a communist. José is the younger brother of Miguel Kast, who was one of the Chicago Boys and President of the Central Bank under Pinochet. Like the rest of us, Chileans live in a world shaped by Milton Friedman.

Sebastian Garren is the founding director of a middle school in St. Louis, Missouri, where he specialises in ancient languages, mathematics, and ethics. You can read his blog here.

Conclusion: Friedman as GOAT?

For someone who lived such a remarkable life, Milton Friedman could be rather unreflective. His memoir, Two Lucky People, which he coauthored with Rose, is extremely unilluminating. Milton was so tone-deaf that he likely had congenital amusia, which he does not think merits a mention. Two Lucky People has also fueled a lot of misconceptions about the evolution of Friedman’s policy views, such as a poorly phrased passage which makes it sound like he was previously a Keynesian. In Jennifer Burns’s account, Friedman’s free-market views cohered early: in the mid-1930s, when he was still in graduate school. On Tyler Cowen’s podcast, Jennifer Burns said one of the reasons why she ended up writing a biography was to “undo the damage” caused by Two Lucky People.

There were many other contributions made by Friedman which we didn’t have time to even mention at the event. Our least excusable omission was a discussion of the permanent income hypothesis. This is important enough that I’ll put some detail in a footnote.43 We also didn’t get to:

Friedman’s influential campaign to abolish the draft and switch to a volunteer army.

His work with Simon Kuznets (he of ‘Kuznets curve’ fame) on the effects of occupational licensing.

His two other TV shows, in one of which you can watch a young David Brooks being converted to conservatism in real time.44

His involvement with party politics, and advising of Richard Nixon, Ronald Reagan, and Margaret Thatcher.45

His occasionally successful efforts to push for constitutional limitations on expenditure and taxes in various American states.

His mentors in the ‘first generation’ of the Chicago school, such as Henry Simons and Frank Knight.

Friedman died in 2006, at the age of 94. Because he lived so long, he forms a remarkable link in the chain of the history of economic thought. He worked on creating a system to report economic statistics during the Great Depression,46 and was also interviewed by Russ Roberts on the EconTalk podcast.